## **How to Find the Best Deals for Your Auto Insurance Dunnville Policy Now**

Securing a reliable and affordable vehicle policy in a small, tight-knit community requires a localized strategy that blends provincial knowledge with rural sensibility. For residents of Haldimand County, navigating the specifics of **auto insurance dunnville** is often a tale of two realities: enjoying some of the most competitive rates in Southern Ontario while simultaneously bracing for a massive legislative overhaul. As of March 2026, the insurance industry in Ontario is standing on the precipice of a "modular" revolution that will fundamentally change how every driver in the Grand River area selects their benefits. Whether you are commuting to Hamilton for work, managing a farm on the outskirts of town, or simply enjoying the scenic routes along Lake Erie, understanding your coverage is no longer just a legal checkbox. It is a vital financial defense. The tranquility of Dunnville’s streets often masks the statistical complexities that insurers use to calculate your premiums, from the frequency of deer collisions to the specific risks associated with highway driving. By mastering the nuances of the local market, you can ensure that your hard-earned money stays in your pocket while your protection remains ironclad.

## **The Regional Advantage and Local Risk Factors in Dunnville**

Drivers in this region typically benefit from a "rural discount" that their urban counterparts in the Greater Toronto Area can only dream of. Because Dunnville has a lower population density and significantly less traffic congestion, the statistical frequency of multi-vehicle collisions is lower. According to current data, the average annual premium for **auto insurance dunnville** sits at approximately $1,394, which breaks down to about $116 per month. This is remarkably lower than the provincial average of $2,779 seen in higher-traffic zones. However, being a rural driver comes with its own unique set of "territorial risks" that insurers watch closely. For instance, the commute distance for Dunnville residents is often higher than average, with many drivers traveling 57 km or more daily for work or essential services. High annual mileage is a primary driver of premium increases because more time on the road directly correlates with a higher probability of an incident.

Furthermore, rural roads present specific environmental hazards that urban policies often downplay. Animal strikes, particularly involving white-tailed deer, are a frequent occurrence in Haldimand County, especially during the dawn and dusk hours. This makes Comprehensive Coverage – the portion of your policy that handles "acts of God" and non-collision events – a non-negotiable addition for most local residents. According to [Wikipedia](https://en.wikipedia.org/wiki/Vehicle_insurance), this type of coverage protects against damage not caused by a collision, such as fire, theft, or contact with animals. While your liability premiums might be low, your comprehensive costs may be slightly higher than expected due to these localized wildlife patterns. Understanding this balance is key to selecting a deductible that makes sense for your specific driving environment.

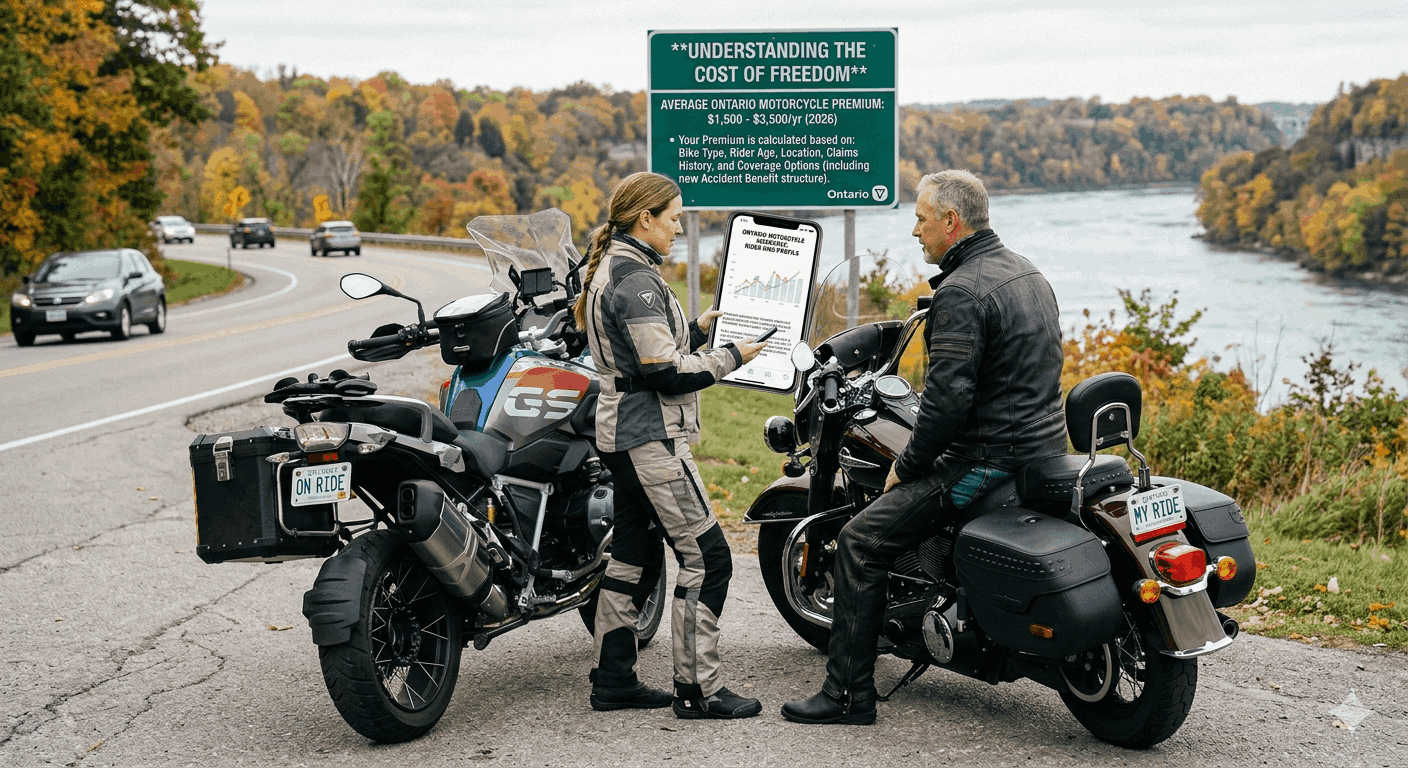

## **Navigating the 2026 Ontario Insurance Reforms**

The most significant change currently facing every policyholder is the provincial shift toward a "modular" or "à la carte" insurance model, set to take full effect on July 1, 2026. For decades, Ontario has mandated a robust package of Statutory Accident Benefits (SABS) that provided automatic support for income replacement, caregiving, and housekeeping. Under the new rules governed by the Financial Services Regulatory Authority of Ontario (FSRA), many of these benefits will become optional. This means that when you renew your **auto insurance dunnville** after July, your policy will only include medical, rehabilitation, and attendant care as mandatory minimums. Everything else, including the vital "Income Replacement Benefit," will require you to actively "opt-in" and pay an additional premium.

This change is designed to give consumers more choice and potentially lower the baseline cost of insurance, but it places a heavy burden of responsibility on the driver. According to reports in [Google News](https://www.google.com/search?q=ontario+auto+insurance+reform+2026+impact), opting out of these benefits might save a driver only about 5% on their total premium, yet it could leave them without thousands of dollars in support if they are unable to work after an accident. For a community like Dunnville, where many residents are self-employed or work in trades without extensive workplace disability plans, these optional benefits are actually essential. If you are a farmer or a small business owner in town, losing your income replacement coverage could be financially catastrophic. It is critical to review your policy documents carefully and consult with a local broker who can explain how these "modular" choices interact with your specific lifestyle and existing health benefits.

## **Strategic Ways to Optimize Your Dunnville Premiums**

While geography works in your favor, your personal "insurance profile" is what ultimately determines if you pay $100 or $200 a month. Insurers use complex actuarial science to predict your risk level based on several controllable factors. According to [Google](https://www.google.com/search?q=how+to+lower+auto+insurance+rates+ontario), one of the most effective ways to lower your rate is by increasing your deductible. By agreeing to pay the first $1,000 or $2,000 of a claim yourself, you signal to the insurer that you are a low-risk client, which can result in a significant reduction in your monthly payments. However, you should only choose a deductible that you can comfortably afford to pay out-of-pocket on short notice.

Another powerful tool for the modern Dunnville driver is "Telematics" or Usage-Based Insurance (UBI). Since many local residents spend a significant amount of time on highways or secondary roads, a telematics device or app can track safe driving behaviors such as smooth braking, gradual acceleration, and avoiding late-night driving. If you are a responsible driver who avoids the "witching hours" between midnight and 4:00 AM, you could earn a discount of up to 25% on your renewal. Additionally, bundling your vehicle policy with your home or farm insurance is a classic but effective strategy. Most providers in the region offer a "multi-line" discount that can shave hundreds of dollars off your total annual bill. Finally, maintaining a clean driving record is paramount. In a smaller community, traffic convictions are less frequent than in the city, and keeping your record "claims-free" is the single best way to maintain your status as a preferred client with the lowest possible rates.

## **Conclusion and Your Next Step**

Finding the perfect balance of price and protection for your [**auto insurance dunnville**](https://theaim.ca/) needs doesn't have to be a daunting task. By leveraging the natural advantages of your rural location and staying ahead of the 2026 legislative changes, you can build a policy that reflects your actual risks rather than just a provincial average. Remember that the "cheapest" policy is rarely the best value if it leaves you vulnerable when you need help the most. As the transition to the new modular system approaches, the best defense is an informed offense. Take the time to audit your current coverage and ensure that your income and family are protected against the unexpected.